I Was Denied a Mortgage Because of Something I Didn't Even Know Was on My Credit Report

“Financial peace isn’t the acquisition of stuff. It’s learning to live on less than you make, so you can give money back and have money to invest.”

— Dave Ramsey

How are things in your world? Have you checked your credit report lately? Like, actually looked at what’s on there? If you’re like most people, you probably haven’t. And that ignorance could be costing you thousands of dollars in higher interest rates — or blocking opportunities entirely.

I used to think credit reports were only for bankers to worry about. Something mysterious that happened behind closed doors when I applied for a loan. Then I discovered a collections account for a medical bill I’d never even received. That single $340 mistake dragged my credit score down by nearly 80 points and almost cost me my first home.

Long story short — I’m going to break down exactly what’s on your credit report, why it matters more than you think, and how to take control of this critical piece of your financial life.

Jennifer R.’s $15,000 Mistake

Jennifer R. had always been responsible with money. Paid her bills early. Never missed a payment. So when she went to buy a new car, she expected smooth sailing.

“The finance manager looked at me with this expression,” she recalled, “and asked if I knew about the judgment filed against me.”

Judgment? Jennifer had no idea what he was talking about. Turns out, a contractor she’d hired years earlier had sued her in small claims court over a disputed bill. She’d moved, never received the court notices, and the case was decided without her. Now it was sitting on her credit report, making her look like a deadbeat.

Because of that judgment, Jennifer’s interest rate was three percent higher than it should have been. Over the life of that car loan, she paid an extra $4,200. On a house, that same credit damage could cost fifteen thousand dollars or more in additional interest.

Knowledge isn’t just power here. It’s money.

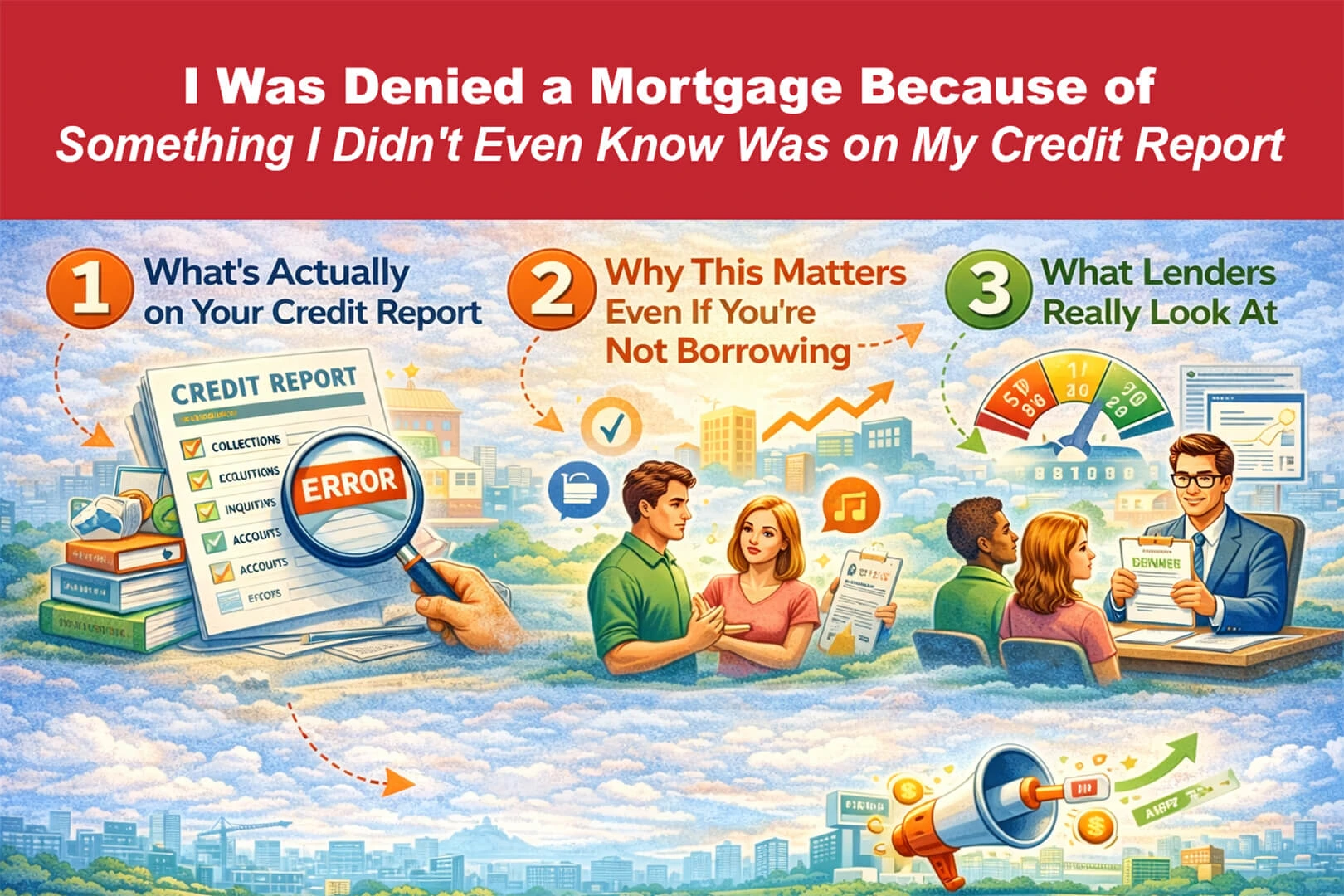

What’s Actually on Your Credit Report

Your credit report is basically a financial biography. Here’s what lenders see when they pull it:

Personal information. Your name, address history, Social Security number. This helps ensure your credit data goes to the right file. If you’ve ever changed your name or moved frequently, this section can get messy.

Account details. Every credit card, loan, and line of credit you’ve ever had. The report shows who you borrowed from, what type of account it is, when you opened it, your credit limit or original loan amount, and your current balance.

Payment history. This is the big one. Every time you’re late — or on time — your creditors report it. Late payments are categorized as thirty to sixty days late, sixty to ninety days late, or over ninety days late. Each category hurts more than the last.

Collections. If you’ve ever been sent to collections for non-payment, that stain sits on your report for seven years. Even medical bills and utility disputes can end up here.

Credit inquiries. When a lender checks your credit, it’s noted. Too many inquiries in a short period can signal desperation and lower your score. These stay on your report for about two years.

Public records. Bankruptcies, judgments, tax liens. The credit bureaus access public records and display them prominently. These are the most damaging items possible.

Why This Matters Even If You’re Not Borrowing

Maybe you’re thinking, “I don’t need a loan right now, so who cares?” Guidance please — your credit report affects way more than borrowing:

Landlords check your credit before approving apartment applications. A poor report could mean a rejected application or a higher security deposit.

Employers in many states can pull credit reports for job candidates, especially for positions involving money or security clearances.

Insurance companies use credit information to set premiums. Bad credit often means higher car and homeowners insurance rates.

Utility companies may require deposits from customers with poor credit history.

Your credit report is your financial reputation. And in today’s world, reputation is everything.

What Lenders Really Look At

Credit reports are important, but they’re not the whole story. When you apply for a loan, lenders also consider your income and employment history to verify you can afford the payments. They calculate your debt-to-income ratio to see how much of your income is already committed to other debts. They look at the length of your credit history and the mix of account types.

A perfect credit score doesn’t guarantee you’ll be approved for everything. But a damaged credit report almost guarantees you’ll pay more for everything — or be denied entirely.

How Jennifer R. Took Back Control

After discovering that judgment, Jennifer got serious about monitoring her credit. She pulled her free reports from all three bureaus and disputed the judgment that she’d never been properly notified about. It took four months and a lot of documentation, but she got it removed.

“I check my credit reports every four months now,” she said. “Once from each bureau, spread throughout the year. It takes fifteen minutes and saves thousands of dollars.”

She also set up alerts for any new accounts or inquiries. “If someone tries to open credit in my name, I’ll know within twenty-four hours. That peace of mind is awesome.”

Your Action Steps Today

First, pull your free credit reports. You’re entitled to one free report from each bureau annually at AnnualCreditReport.com. Do it today.

Second, read every line. Look for accounts you don’t recognize. Check that payment histories are accurate. Note any collections or public records.

Third, dispute any errors. The bureaus have a process for this. It takes time, but it works. Document everything.

Fourth, set up monitoring. Many banks and credit cards offer free credit score tracking now. Use it.

Remember: if you don’t take good care of your credit, your credit won’t take good care of you. Learned behaviors can be unlearned. Even if you’ve made mistakes in the past, today is the day you take control.

Your financial future is worth fifteen minutes of attention. Go check your report.

Hugs, Love and Prayers,

Larisa